Market Report

Learn more about all important trends in the precious metals markets in our market reports on a regular basis.

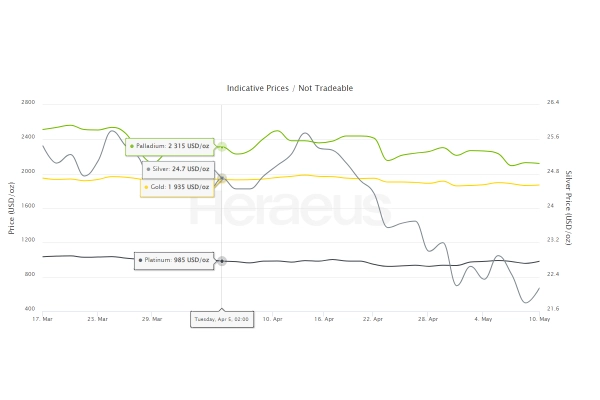

Platinum Breaks 2021 High, Hits 10-Year Peak

No. 22 | 23rd June 2025

The Fed follows form. In last week’s meeting of the Federal Open Market

Committee (FOMC), US baseline interest rates were held firm at 4.5%,

which was in line with expectations. What is beginning to change, however,

is the outlook for the rest of the year. Two camps are beginning to emerge:

those in the committee who believe there should be 50 bp of cuts before

year-end, and those that see rates staying where they are. The emergence

of the latter since the last FOMC meeting helped to strengthen the dollar

somewhat.

Register for our Market Report

You would like to receive our market report by e-mail? Then register now using the form provided below.

After submitting the form, you will receive an activation link via e-mail. Please confirm your registration by clicking on the link. You can, of course, withdraw this consent at any time. At the end of each newsletter you will find a corresponding unsubscribe link.